On June 13, at the 2025 SMM (13th) Minor Metal Industry Conference—Antimony Forum hosted by Shandong Humon Smelting Co., Ltd. and SMM Information & Technology Co., Ltd., SMM PV industry analyst Tianhong Zheng delivered a presentation titled "Current Status and Trends of the PV Glass Industry."

Current Domestic PV Glass Price Situation

China's PV Glass Price Status and Review

In 2025, China's new PV glass capacity increased rapidly due to favorable market conditions earlier, but after a short-lived demand surge, supply and demand once again showed signs of mismatch, leading to a price trend that first declined and then rose.

►PV Glass Price Trend

From January 2025 to the Chinese New Year period, domestic module demand began to decline as the installation rush season ended. Against the backdrop of weakening module scheduled production, rising winter natural gas prices provided some cost support, coupled with production cuts due to blocked glass outlets, resulting in an upward trend in glass transaction prices.

After the Chinese New Year, end-use demand was quickly driven by the "430" and "531" policies. Module scheduled production, especially for distributed PV modules, rose rapidly, with planned production reaching nearly 60GW. Meanwhile, glass supply declined due to the impact of cold repairs on previously blocked furnaces, accelerating destocking speed and pushing glass prices higher.

From March to April, the glass price rally slowed down. This was mainly because, as the glass market improved, many previously built but uncommissioned furnaces began concentrated start-ups, and previously blocked furnaces resumed large-scale production. Although overall supply remained tight, potential price risks gradually emerged. Additionally, module prices started to decline slightly from April, indicating weakening demand support.

From May to present, module scheduled production began to decline, and policy-driven demand started to pull back. Module prices entered a downward trajectory, putting significant pressure on glass prices. Glass prices fell multiple times in succession, rapidly approaching cost levels, with further declines expected.

Changes in Global PV Glass Supply

Overall Global Supply Landscape

In recent years, domestic supply has become relatively saturated, leading to a slowdown in growth. However, there remains substantial idle capacity awaiting deployment, suggesting considerable potential for future expansion.

In H1 2025, driven by the "430" and "531" policies, module scheduled production rose rapidly, accelerating glass price increases. Some idle capacity began start-ups, speeding up supply-side expansion.

Analysis of China's PV Glass Supply Side (Provincial Capacity Expansion)

Currently, PV glass capacity is mainly concentrated in provinces like Anhui and Jiangsu, which have advantages in quartz sand raw materials and large downstream module capacity. Future development of China's PV glass enterprises will also consider provincial energy consumption restrictions, expanding to regions like Guangxi with surplus energy capacity.

Currently, PV glass capacity is mainly concentrated in provinces such as Anhui, Jiangsu, and Guangxi, which are close to raw material sources and have strong downstream module support. Additionally, regions with top-tier enterprises will also be the main areas for future capacity additions.

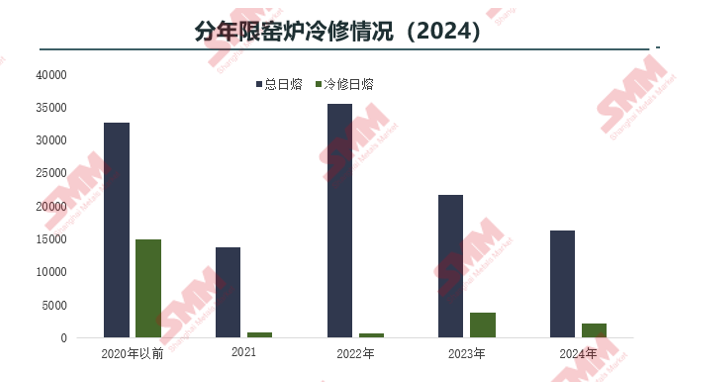

Analysis of China's PV Glass Supply Side (Provincial Capacity Shutdowns and Production Cuts Review)

Since Q3 2024, market conditions rapidly cooled, leading to increased frequency of kiln shutdowns, cold repairs, and production cuts.

Analysis of China's PV Glass Supply Side (Detailed Review of Production-Cut Kilns)

Leading enterprises took the lead in cutting production, restoring industry supply to a rational adjustment phase.

From the perspective of cold-repair kiln lifespans, although cold repairs surged unprecedentedly in 2024, over 70% of the kilns were built and put into operation before 2020, primarily due to approaching equipment lifecycles. Kilns cold-repaired after 2023 were those with complete procedures such as indicators and capacity replacements, allowing them to resume production post-repair. Kilns lacking procedures must supplement documentation before restarting. Additionally, most newly built kilns undergoing cold repairs in 2024 were operating at low temperatures due to weak market conditions, resulting in lower output. These kilns had lower production costs and opted for cold repairs under profit pressure.

In 2024, leading enterprises conducted significant cold repairs and production cuts. Although they were not the first to initiate cuts, recent plans still include substantial reductions. Due to declining module demand, the two industry leaders still plan nearly 3,000 mt/day of production cuts in December, with some large enterprises also planning further reductions.

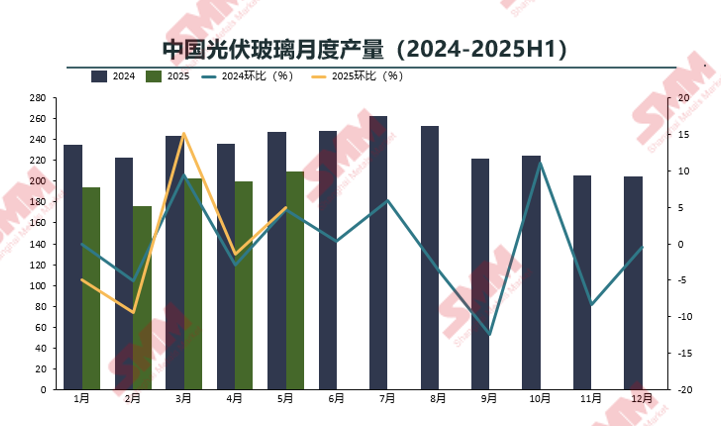

Analysis of China's PV Glass Supply Side (Monthly Production Trends)

Leading enterprises took the lead in cutting production, restoring industry supply to a rational adjustment phase.

PV glass production in 2025 is expected to drop significantly due to earlier kiln shutdowns and production cuts. Despite new lines coming online in H1, domestic glass enterprises are likely to continue shutdowns and cuts as market conditions weaken, making it unlikely for production to exceed 2024 levels.

Glass prices are expected to decline further in June, approaching cost lines, prompting enterprises to plan production cuts and cold repairs under operational pressure and future trends.

Analysis of Overseas PV Glass Supply Side

Due to abundant overseas ore and labor resources, as well as policy avoidance, overseas glass capacity has grown rapidly in recent years, mostly through domestic enterprises establishing factories abroad. However, tightening overseas policies and increasing self-production by foreign enterprises are expected.

Currently, overseas PV glass capacity is mainly concentrated in Vietnam, Malaysia, and India, where raw materials are convenient and competitively priced, with strong downstream module support. Future capacity additions will likely focus on regions with module enterprises and fast-growing PV markets like Europe and the US, with new capacity under planning in Canada and the Middle East.

Analysis of Demand Trends at Home and Abroad

Global PV Market Demand

Under a neutral outlook, the global market size for new PV installations is expected to reach 562 GW in 2025.

The Middle East and Africa regions will maintain double-digit growth, while South America will shift to negative growth.

►SMM Commentary

Asia-Pacific Region (excluding China): India's Production-Linked Incentive (PLI) scheme and the ALMM module list impose requirements for local manufacturing to meet local consumption. SMM anticipates significant growth in India in 2025 and 2026, with a gradual slowdown in growth from 2027 to 2032 according to India's National Energy Plan. Indonesia has emerged as the fastest-growing market in Southeast Asia, with plans to add 4.7 GW of new solar installations by 2030 under the local Electricity Procurement Plan (RUPTL).

Europe: Germany implemented the "PV Peak Law" in February, suspending subsidies during negative electricity price periods, which has hindered the largest market in Europe. The localization process of the Net Zero Industry Act (NZIA) has been impeded by raw material supply issues, making it difficult for many plans to be implemented.

Americas: In North America, the average annual new installations in the US, Canada, and Mexico will stabilize between 51-53 GW from 2026 to 2030. In South America, Brazil's weak power infrastructure poses challenges for PV transmission and distribution, leading to an overall negative growth trend in the region.

Middle East: Saudi Arabia has proposed the "Vision 2030," the UAE has launched multiple PV projects, and other Gulf countries are actively pursuing clean energy transitions. The Middle East's natural advantage of high solar irradiance makes it the PV market with the greatest growth potential.

Africa: After experiencing a contraction in the South African market and delays in North African project development in 2024, Africa has announced approximately 40 GW of new projects, which, along with previously delayed projects, are expected to be connected to the grid by the end of 2025, particularly tender projects in Algeria. SMM expects a relatively high compound annual growth rate from 2025 to 2028, with a slowdown in growth from 2029 to 2030 due to factors such as high financing costs and insufficient power grid infrastructure.

Current Operating Status of Chinese Modules

China's PV module inventory levels are relatively reasonable, with room for a rebound after the decline.

In 2025, module supply will begin to cut production from May, and weakening demand will lead to a significant supply-demand mismatch for modules. Based on the current supply and demand situation for modules, inventory levels are relatively low, with module inventory reaching its lowest point of the year in May. Inventory buildup may continue subsequently. After experiencing the low point in industry chain prices, module prices still have resilience for a rebound.

Currently, the costs of integrated enterprises and specialized module enterprises are inverted, with losses occurring in all segments of main materials. The overall cost of auxiliary materials is high, exceeding that of main materials. Non-silicon costs have become the lifeline of enterprises, making the overall module segment the most profitable, primarily determined by the supply-demand pattern. Subsequently, integrated enterprises will take proactive measures to ensure a relatively advantageous position.

Global Outlook for Future PV Module Market

Overseas Demand Share Continues to Rise, Distributed Installations Expected to Accelerate

In a phase of general supply surplus, the overall expansion rate of PV module capacity is expected to slow down from 2024 to 2027. PERC capacity will gradually be phased out by the market, with TOPCon capacity taking the lead. Future capacity increments will mainly come from new investments and expansions in new technology routes, including HJT, BC, lightweight flexible modules, thin-film modules, etc. After 2026, with the maturation of perovskite technology, a new round of module production will commence.

Major PV markets globally, including India, the US, and Europe, have expansion plans for their domestic PV module capacities. It is expected that most of these capacities will be fully operational by 2026.

The share of China's new installations is declining year by year. Traditional regions are experiencing weak demand and saturated inventory cycles, with no immediate potential for explosive growth. Emerging countries such as Saudi Arabia and the UAE are becoming the main drivers. It is expected that overseas centralized installations will surpass domestic centralized installations in China this year.

In terms of distributed installations, with the construction of new power systems and the national focus on implementing the "Thousands of Households Embracing Solar" initiative to explore and promote the clean and low-carbon transformation of rural energy, the future application of distributed PV will become more widespread and in-depth. Integration with various industries will become closer, and it will form integrated development with technologies such as ESS and smart power grids. Therefore, future distributed demand will remain a stable increment in PV demand, but an expected slowdown in expansion is also anticipated from 2027.

》Click to view the special report on the 2025 SMM (13th) Minor Metals Industry Conference

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)